MCA Relaxes Additional Fees for DPT-3 Filing

MCA Relaxes Additional Fees for DPT-3 Filing up to 31 July 2026

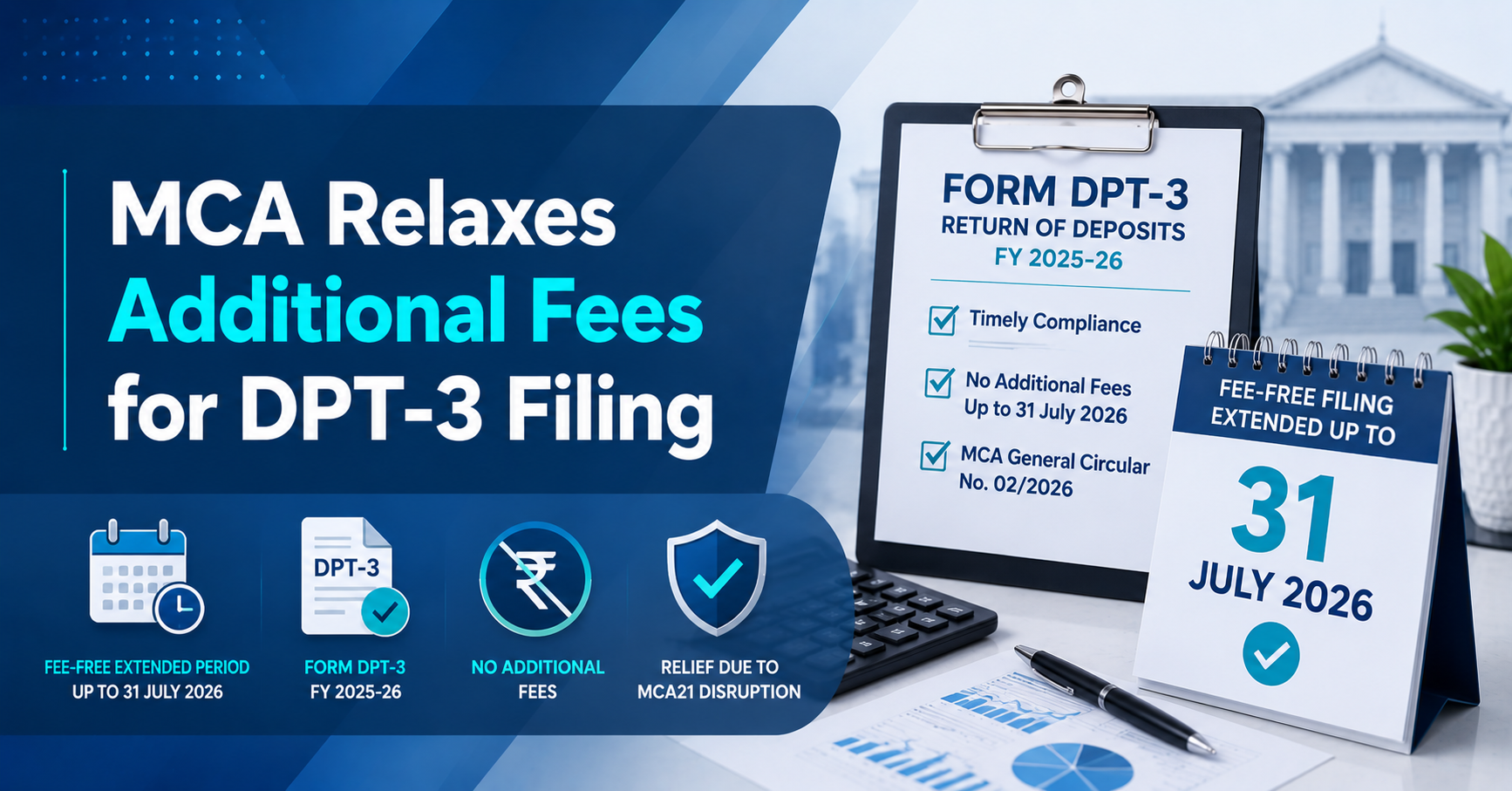

The Ministry of Corporate Affairs (MCA) has provided significant relief to companies by allowing Form DPT-3 for the financial year 2025-26 to be filed up to 31 July 2026 without payment of additional fees. This one-time relaxation has been granted due to the disruption caused by the MCA21 data centre restoration activities following the fire incident on 5 June 2026. (Simpliance)

Background of the Relaxation

Under the Companies (Acceptance of Deposits) Rules, 2014, companies are required to file Form DPT-3 (Return of Deposits) annually.

For FY 2025-26:

-

Original statutory due date: 30 June 2026

-

Fee-free filing period extended up to: 31 July 2026

-

Relief granted through: MCA General Circular No. 02/2026 dated 19 June 2026. (Simpliance)

Need help with this? Talk to A. S. Darve & Co. →

What Relief Has MCA Provided?

The MCA has clarified that companies filing Form DPT-3 on or before 31 July 2026 will not be required to pay additional (late) filing fees, even though the original due date remains 30 June 2026.

This relaxation has been introduced because MCA21 services were impacted during the data centre restoration process undertaken after the fire incident. (Simpliance)

Important Clarification

It is important to note that:

-

The statutory due date continues to remain 30 June 2026.

-

The circular does not extend the statutory due date.

-

It merely waives the additional filing fees for forms filed up to 31 July 2026. (taxupdate.in)

Who is Required to File Form DPT-3?

Form DPT-3 is generally required to be filed by companies having outstanding amounts that qualify as:

-

Deposits accepted by the company; or

-

Amounts not considered deposits but reportable under the Companies (Acceptance of Deposits) Rules, 2014.

Subject to the applicable exemptions, the filing requirement extends to most companies having reportable outstanding receipts as on 31 March 2026. (Mas LLP)

Action Points for Companies

Companies should:

-

Review whether Form DPT-3 is applicable.

-

Reconcile outstanding deposits and exempt borrowings as on 31 March 2026.

-

Prepare the necessary disclosures and supporting information.

-

Complete filing well before 31 July 2026 to avoid last-minute portal congestion.

-

Preserve the SRN and acknowledgement after successful filing. (Mas LLP)

Why Timely Filing Matters

Although additional fees have been waived during the relaxation period, companies should not postpone compliance. Filing within the extended fee-free window helps:

-

Avoid additional filing fees after 31 July 2026.

-

Maintain good corporate compliance records.

-

Prevent future regulatory complications relating to deposit reporting.

-

Ensure smooth ROC compliance for FY 2025-26. (Simpliance)

Conclusion

The MCA's one-time relaxation under General Circular No. 02/2026 provides welcome relief to companies affected by the MCA21 disruption. Eligible companies should utilize the extended fee-free window and complete their DPT-3 filing well before 31 July 2026 to ensure timely compliance.

For expert guidance on this topic, contact your tax professional today.

EXCERPT: MCA has allowed Form DPT-3 for FY 2025-26 to be filed up to 31 July 2026 without additional fees due to the MCA21 system disruption.

SEO_TITLE: MCA Extends DPT-3 Fee-Free Filing to 31 July 2026

SEO_DESCRIPTION: File Form DPT-3 for FY 2025-26 by 31 July 2026 without additional fees under MCA General Circular 02/2026. Contact a tax professional today.

Have Questions? We're Here to Help

Get expert advice from A. S. Darve & Co.. Reach out to discuss your requirements.